Europe must invest in the critical raw materials sector to develop its own strategic autonomy and to re-industrialise key industrial ecosystems

By Bernd Schäfer, Bernd-Schäfer-EIT-RawMaterials-CEO

Critical raw materials are key enablers of the green and digital transition and are now of critical importance to preserving the global competitiveness of the EU’s most strategic economic sectors. They are fundamental for the EU to develop its own strategic autonomy, and to re-industrialise key European ecosystems. In particular, critical raw materials are crucial for transforming the EU energy system towards a CO2 neutral energy production and to achieve the target of reducing net greenhouse gas emissions by at least 55% by 2030.

The development of renewable energy systems will require unprecedented supplies of critical raw materials. Europe is rich in raw material resources, for example, a total of 14 projects from mine and ‘urban mines to magnet’ were identified by the European Raw Materials Alliance (ERMA).

These projects could form the foundation of a European rare earths industry, capable of delivering at least 20 percent of EU demand for raw materials by 2030.

There are countless other reserves of raw materials throughout Europe, that are yet to be utilised, that is, natural resources as well as urban mine resource potentials. But it is the access to sustainable raw materials from mining which is of paramount importance to enable the quick turnaround of a massive industrial and societal transition aiming for minimising greenhouse gas emissions and the reduction of the impacts that cause global warming.

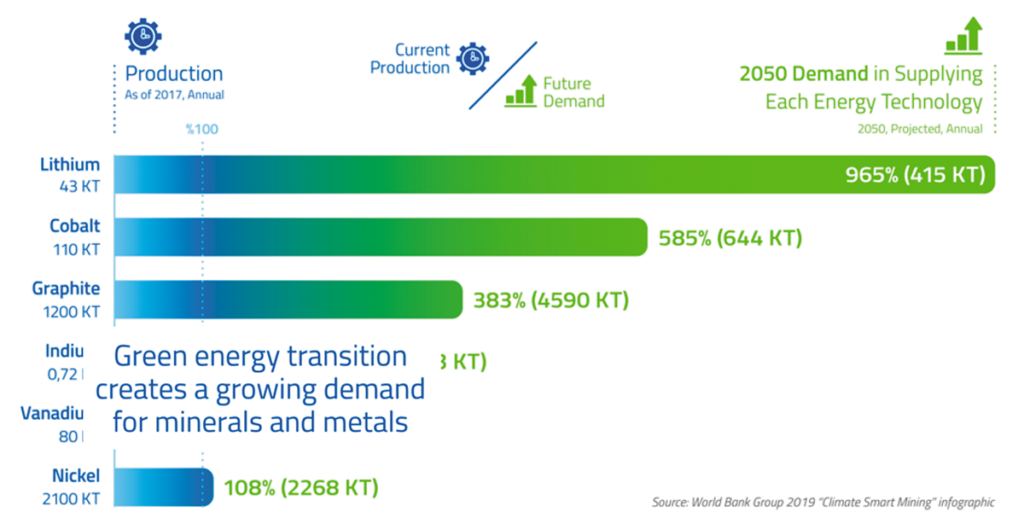

A 2020 World Bank Group report finds that the production of minerals, such as graphite, lithium and cobalt, could increase by nearly 500% by 2050, to meet the growing demand for clean energy technologies. It estimates that over 3 billion tons of minerals and metals will be needed to deploy wind, solar and geothermal power, as well as energy storage, required for achieving a below 2°C future (Source: Worldbank.org). For e-car batteries and energy storage alone, Europe will for instance need up to 18 times more lithium by 2030 and up to 60 times more by 2050 (Source: EC, Critical Raw materials for Strategic Technologies and Sectors in the EU, A Foresight Study, 2020).

Europe’s strategic dependencies and the key actions we need to take are well-described in the Critical Raw Materials Action Plan of the European Commission and their 2020 New Industrial Strategy. A more specific Action Plan on Rare Earth Magnets and Motors has been developed under the umbrella of ERMA, i.e., together with a wide stakeholder group involving industry, academia, and wider society.

Both the covid-19 pandemic and the current geopolitical issues we face in Europe now have shown that the lack of a European mining industry as well as the lack of sustainable supply of secondary critical raw materials, has rendered Europe more vulnerable to supply chain disruptions and shortages. For example, in 2020 China provided more than 98% of the EU’s need of rare earth elements and 93% of Magnesium, Turkey provided 98% of the EU’s need of borate and South Africa provided 71% of the EU’s need for platinum. Additionally, China, Turkey and South Africa are all economies whose environment, social and governance (ESG) standards substantially differ from European ones which therefore, also carries an element of risk.

The current shortages and supply disruptions of other critical raw materials, like the predicted magnesium shortage, raises the risk for EU industries. The subsequent price inflation may be only a minor problem, in comparison to the cost of not having available raw materials at all.

Europe has what it takes to lead the Green transition globally

In light of the tragic European geopolitical events unfolding at the time this article was written, the ability for Europe to set up inter-European value chains between EU member states and further afield is more urgent than ever. For example, rare earths mined in Sweden or Norway can be processed in Estonia and Poland; manufactured into magnets in Estonia, Germany and Slovenia; to be used in cars built in France, Germany, or Sweden. Europe must also diversify its supply chains with other resource-rich countries by establishing new trade and cooperation agreements.

Europe can also establish financing arrangements using both, public and private finance. Recently launched public funding tools include the Just Transition Fund, the Innovation Fund, and the so-called Important Projects of Common European Interest (IPCEI).

Europe has shown in other business areas that common standards, for example, around recycling, can change behavior and drive innovation. European industry must invest not only in primary raw materials extraction but also in the development of advanced materials, smart product designs, and refining and recycling facilities, which are critical to secure a dependable supply of secondary raw materials, mostly from industrial actors.

The role of ERMA and EIT RawMaterials

In September 2020, ERMA was launched by Commissioner Breton and Vice-President Šefčovič with the aim of making European industrial ecosystems economically more resilient. ERMA, (which is managed by EIT RawMaterials), is therefore firmly embedded in the European Commission’s policy framework.

ERMA’s community of currently 600 stakeholders of businesses, governments, start-ups, R&D, NGOs and academia partners regularly consult to identify regulatory bottlenecks as well as a number of substantial investment opportunities. Qualifying entities and organisations are able to become members of ERMA in order to take advantage of connecting across the entire stakeholder base to form new, sustainable industrial ecosystems. By anticipating key eco system raw materials needs, ERMA defines priority activities and groups them in so called ‘Clusters’ in which information is exchanged and policy suggestions are developed. So far, an action plan has been issued for the Rare Earth Magnets and Motors Cluster and 30 pre-screened projects have been identified for strategic investment in this area, worth more than 10 billion euros.

Supporting business innovation is a primary focus at EIT RawMaterials. European innovation is already setting a new world standard which is making mining more attractive as an industry from both a business and a workforce perspective.

The advanced technologies developed include equipment automation, digital tools and battery powered equipment. For example, Epiroc, a battery-electric equipment producer, is committed to halving CO2 emissions from the downstream use of their equipment as well as from their own production lines and transport, by 2030.

At EIT RawMaterials, we place great strategic focus on providing the right tools to boost the potential for European startups. To date we have worked with over 360 start-ups that contribute to one of our strategic priorities. These priorities include securing raw materials supply, designing material solutions, or closing materials loops. Each year at the EIT RawMaterials Summit in Berlin, start-ups are introduced to established businesses, investors, politicians, and entrepreneurs.

Education is another key focus area for EIT RawMaterials. European education institutions must become more aligned with raw materials industrial requirements and advancements. In fact, with institutions like TU Bergakademie Freiberg and Kungliga Tekniska Högskolan (KTH), Europe has the longest academic educational history in mining and metals in the world. EIT RawMaterials has signed on 70 partner universities who are collaborating with leading business entities across the entire value chain within R&D and curriculum design. The EIT RawMaterials Academy provides for an entire ecosystem of learners ranging from PhD students, Masters’ students, industrial partners, professionals within the raw materials sector and wider society. Already 200,000 students have experienced the benefits of its education offerings.

Why does this focus on innovation, education and investments matter? According to Eurostat projections, seven core strategically important ecosystems that are reliant upon domestic raw material supply, could represent as many as 32 million jobs by 2030 in Europe. Securing these jobs requires a skilled workforce, innovative approaches, and strategic investments in Europe along the entire raw materials value chain.

With these bold, appropriate and ethical actions, Europe can become the most secure, and sustainable global provider of critical raw materials. But we must act now.