EU Green Deal Industrial Plan – More muscle, more speed and more simplicity for EU strategic industrial value chains

By Diego Pavia, CEO of EIT InnoEnergy

The global race for climate technologies has accelerated in recent months with major economies ramping up dedicated policies and support schemes. China, the USA, India or South Korea have chosen different approaches for their industrial strategies, but all target the same objective: localise strategic industrial value chains that are needed for the climate transition and are among the biggest drivers for growth in the current and future economy.

Europe’s ambition to remain the early mover and powerhouse in the fight against climate change depends on a strong industrial position in climate technologies manufacturing.

The EU has solid fundamentals to build on but it must beef up its toolbox to boost domestic industrial manufacturing: more muscle, more simplicity and more speed are needed to win this race.

The EU has a strong business case for investors in climate technologies, with highly distinctive features: A legally binding commitment to achieve a net-zero economy by 2050 and an unmatched regulatory framework for the energy transition, a European single market with a mature demand from business or citizens for climate technologies and sustainable products, as well as a robust industrial capacity in many areas.

Also, Europe has demonstrated its ability to pool together its resources when the ambition and objectives are clear, and a fresh approach is properly executed, at speed: A clear example is the European Battery Alliance, which the European Commission mandated EIT InnoEnergy to lead in 2017, and where we now are ahead of the initial ambition of creating a new annual GDP of 250B€ across all the value chain, from mining to recycling.

In addition, the EU can count on a rich industrial innovation ecosystem in climate tech which EIT InnoEnergy, amongst others, has and is contributing to grow. Since 2010, EIT InnoEnergy, as an investor and accelerator, has grown a portfolio of 180+ start-ups and scale-ups, all contributing to the energy transition with made-in-Europe technologies to create maximum impact. A vast majority are CAPEX intensive and looking at developing industrial manufacturing capacities across the value chains of climate technologies (batteries, PV, green H2, wind,…). These companies (amongst them 3 out of the 31 global unicorns in climate tech) are industrial frontrunners in their respective fields (such as NorthVolt in the full life cycle of batteries, H2 Green Steel, GravitHy in decarbonized iron and steel or NexWafe in wafers for Solar PV). They have an aggregated need of EUR160bn of extra financing until 2030 to meet their industrial objectives. This is a tremendous technology and industrial leadership opportunity for Europe that delivers growth and jobs.

From that perspective, the EU is in a privileged position. We have the technologies we need, and the entrepreneurs to create worldwide climate tech industrial champions.

However, the EU’s business case for nvestors and industrialists is hampered by a harsh and long-standing competitiveness gap and by the inability to maintain a level playing field with global players. This is currently amplified by increased electricity prices in Europe and the roll-out of support schemes across the globe such as the US Inflation Reduction Act.

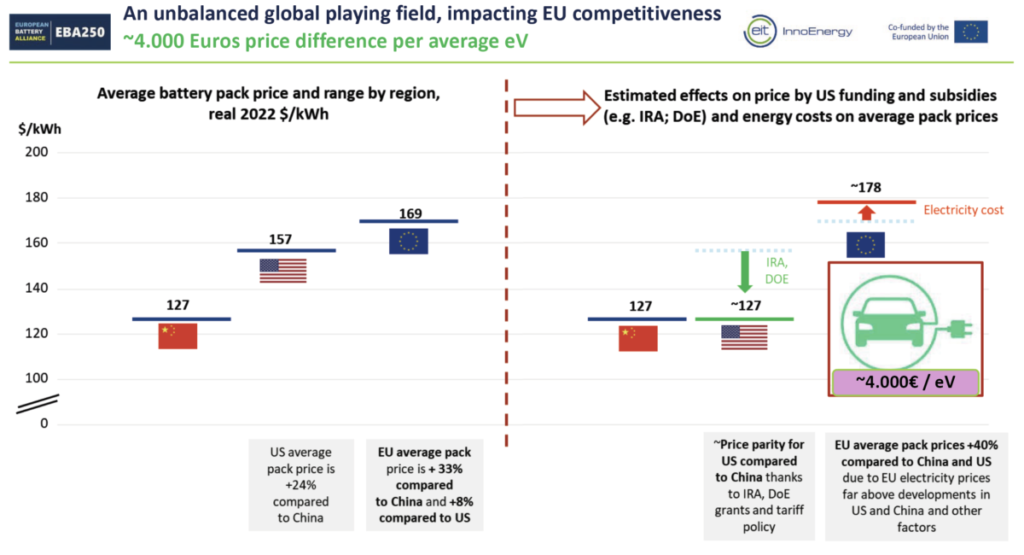

Taking the battery value chain as an example, the situation has become worrisome. The growth, and progress towards a resilient value chain across all segments is endangered. The figure below shows a 50$ disadvantage on a base of 127$ at the battery pack level. This puts European industrial leaders in battery manufacturing in a losing position, and leads them to strongly assess moving their next investment across the pond.

On a similar note, there is a tremendous business opportunity to capture the EU demand for solar PV. The EU deployed more than 40GW of solar PV panels in Europe in 2022. Almost all were imported from China. This equals around EUR12bn of yearly trade deficit for Europe, which is expected to grow even more as demand increases (even if just to meet RepowerEU ambitions). The EU, through the ESIA (European Solar Industrial Alliance), also mandated to InnoEnergy, has set the ambition to develop 30GW of EU domestic PV manufacturing capacity, from ingots to recycling. There is a strong appetite from the industry and investors to seize this business opportunity. Already, a very good pipeline of industrial projects has emerged. Still, the challenge is immense, because it is a scale game, and only beyond 5GW the business cases are viable. Here again there is a competitiveness gap stemming from energy prices, limitation of equipments/machinery, funding gaps, uneven playing field in terms of sustainability of products, and public procurement criteria.

The EU can be the global leader, but this requires being bolder in creating favourable conditions for industrial scaling up.

The EU Green Deal Industrial Plan comes at the right time, with mostly right measures proposed by the European Commission in the Net Zero Industry Act and the Critical Raw Materials Act. It can be made much stronger, with a few targeted additions for speed and simplicity, answering to the needs of the industrial frontrunners:

- Put sustainability, traceability and circularity (recycled content) at the core of the EU industrial strategy for climate technologies. This will ensure that in Europe, to be competitive, any party would have to be performant not only on price but also on traceability, sustainability and recycled content in products. A crystal-clear signal will keep and attract to Europe the right players and the right investors. There are precedents in the EU demonstrating the relevance of this approach: Product regulation setting sustainability criteria and a traceability scheme (such as the EU battery regulation), improved ecodesign rules, the EU ETS (with free allowances earmarked for the best performers) and the associated Carbon Border Adjustment Mechanism. New, simple measures could be added, such as a “sustainable production bonus”. For selected net-zero products, a “bonus” could be granted to manufacturers which overachieve the objectives, or anticipate the provisions, for example of the EU battery regulation or upcoming similar ones for other climate tech products. The incentive will take the form of a grant, made available to the best performers. Compared with the US IRA production incentive, coming without sustainability strings attached, it will confirm the EU’s stance: Leading on sustainability in the world.

- Support strategic industrial projects with best-in-class tools. Setting capacity objectives, be they manufacturing capacity targets for strategic product/technologies or extraction, or processing and recycling targets for strategic raw materials, gives a strong market signal. For industrial projects that will deliver upon those targets, time is of the essence. Both the European Battery Alliance and European Solar PV Industry Alliance have identified a readily available list of credible industrial projects that have the maturity to start operations as early as 2025 or 2026, provided investors get the required signals. Reducing time to permitting, getting effective financial support is required now, not in a year’s time. Therefore, there is no time to lose to label Strategic European Projects that ensure that those targets are met.

Member States now have the possibility to deploy new EU funds and thanks to the recently published and highly welcomed framework for State Aid, national aid without undue delay. Let’s deploy this public support efficiently and at speed to de-risk private investments, which are always doing the heavy lifting. On permitting, the legislative work on the two Acts will be decisive to improve how permit granting is delivered. The ambition must be to bring the EU at the level of global best practices (6 to 9 months for industrial permitting in the US or Canada). For projects already engaged in a permitting process, there should be an urgent effort to accelerate: It is all about administrative capacity and prioritisation of resources. The EU and the Member States should agree on an emergency action. Thinking out of the box, speed could be achieved through a special EU task force of experts mobilised upon need for the permitting of strategic projects, hereby supporting but also building the capacity of local authorities. - Solve the skills gap, now. A value chain is as strong as its weakest link. For most value chains in climate technologies, skills remain a strong bottleneck and a risk for industrial project development. With the European Battery Alliance Academy, an initiative taken by EIT InnoEnergy, the EU has a proven tool to deploy training at the speed and scale required by industry. Replication of this approach to other value chains and creating synergies across different academies makes a lot of sense. That said, the criticality remains the availability of financial support from public authorities to fund training programs, so industry can get the right workers for their needs. A decisive move would be to commit Member States to earmark and frontload a given percentage of their European Social Fund Plus allocations to specific value chains (for instance, 2% for the battery value chain in the next 3 years).

We are in a unique moment in the world and European history. Let’s capitalize on Europe’s early mover advantage in the green transition, and not being shy on leveraging extensively the existing and new tools of the tool box. The business opportunity to be captured has a tremendous impact for Europe in terms of sustainability, growth and jobs. Our next generations deserve that we go the extra mile at speed. EIT InnoEnergy is gearing up for this.