Paving the way towards an affordable and resilient European decarbonization

By Claire Waysand, Executive Vice President, General Secretary of ENGIE

Decarbonizing the European economy and paving the way towards net zero is no longer a choice, but an imperative. The latest IPCC report is very clear, and the UN Secretary General Antonio Guterres even more: it is a code red for humanity.

The European Union has set a clear trajectory with its Climate Law: by 2030, GHG emissions must be reduced by 55% (compared to 1990) and by 2050, emissions must be “net zero”. It is now up to us, European companies, European governments and decision bodies, citizens, to enable this path to become a reality.

At ENGIE, the trajectory is crystal clear with a commitment to Net Zero Carbon by 2045 on all scopes, supported by an acceleration in our development of renewables and in our contribution to the decarbonation of our customers through investments, such as district heating and cooling networks, and through Ellipse Platform, recently launched.

We will invest €15-16 billion by 2023 to reach these objectives. It is just a starting point.

The challenge and the issues at stake are such that we cannot lose time and deviate from the trajectory: 2030 is already tomorrow, in terms of investments and projects deployment. At ENGIE, we have identified a number of essential drivers drawing the path towards the “55%” target first and, later on, the net zero objective.

1. An energy and climate policy that unites rather than divides.

In spite of long debates and difficulties, European policy in this area has always managed, to bring Member States together. The 55% GHG reduction is a shared target. Decarbonizing the EU must be a common cause, carried out while respecting the rights and obligations of Member States. Raising the ambitions in terms of energy efficiency and renewable energies is absolutely essential. Different European Member States will have different ways to reach their targets – which should be respected, as long as they lead to the agreed decrease in GHG emissions. Affordability of the decarbonation path will be critical – as clearly illustrated by recent tensions due to high energy prices. So will its resilience and Europe needs to make sure that the resulting energy mix from national Member states choices meets the decarbonation target, ensuring the security of supply.

2. Rely on a mix of solutions capable of accelerating the decarbonization of the economy.

Decarbonization will require a mix of options used in synergy with the whole energy system: there is no time for cherry-picking. The Climate Target Plan published in September 2020 by the European Commission shows that “at least 55% target” by 2030:

1) is feasible;

2) will put us on the right trajectory towards climate neutrality;

3) requires more effort and contribution of all sectors of economy.

Energy efficiency and renewable electricity will be key. To illustrate, let’s put the renewable targets into perspective. 40% RES in total consumption by 2030 implies up to 450 GW wind by 2030 (180 GW today).

Similarly, solar capacity would have to increase from ~ 140 GW today to up to 375 GW by 2030. The challenge is so huge that it calls for a mix of solutions. In particular, renewable gases (like biomethane or renewable hydrogen) will have a key role to play to exploit synergies and circularity. Unlike intermittent renewable electricity generation they have the great advantage of being storable and dispatchable. Needless to say , renewable heat/cold should also be part of the toolbox, along the development of energy storage and flexibility instruments to cope with a more dynamic energy system.

3. Decarbonizing is a must. It is even better in a cost-efficient manner.

The cost of the energy transition should be kept under scrutiny. Each € will be precious to deliver additional investment capacity. In a sector where relative prices have dramatically evolved in the last decade, doors must remain open to diversified solutions. Solutions that rely excessively on one type of energy only are likely to be too costly and too risky. Diversity is the key to an affordable, reliable and sustainable transition.

Therefore any possibility to exploit synergies and lower costs for consumers (households and industrials) should be leveraged, esp. in a post-crisis context.

As mentioned by the Commission in its energy system integration strategy, cost-effectiveness is indeed crucial. The recent rise in energy prices and the emerging fears of continuing issues for the coming winter illustrate that the prices and availability of energies are essential for the competitiveness of European industry as a whole and for individuals.

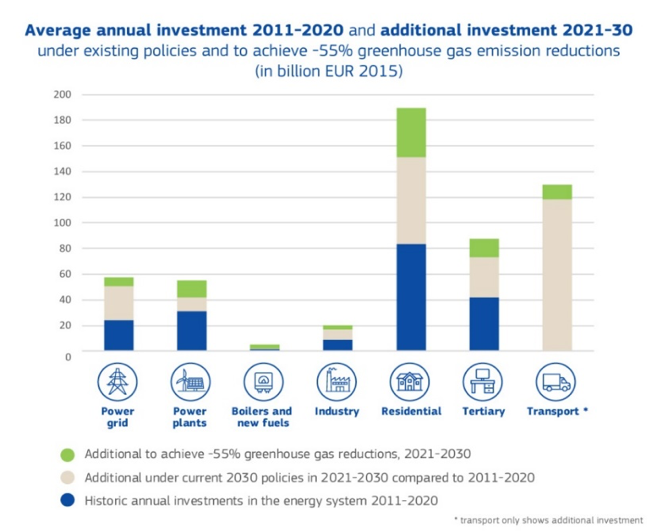

4. Unlocking investment.

The recovery plans seize the opportunity of the economy “restart” to focus on the energy transition, but they will by far not be sufficient. Other measures that will create a funding pipeline for the transition – State aids, Important Project of Common European Interest (IPCEI), Next Generation EU, European Funds – must also contribute to the key goal of reaching 55% GHG reduction by 2030.

However, public money will only contribute to a small proportion of the funding needs. This is why a well-designed taxonomy is important in order to channel private investment. Natural gas can help decarbonize massively, quickly and efficiently the energy mix in a number of European Member States. In its 2019 “The Role of Gas in Today’s Energy Transitions” report, the IEA estimated that (under some market conditions) existing gas capacity could step in to replace up to half of the European Union’s coal-fired power and that this would save around 220 Mt CO2, equivalent to 20% of the European Union’s power sector emissions. In this respect natural gas should be regarded as a transitional energy and accepted as such.

Regulatory measures can also contribute to unleashing investment in nascent sectors. Indeed, gas will of course need to green itself – thanks notably to biomethane and renewable hydrogen (H2) – and well-designed regulation could support the Commission objective to get 40GW of Green H2 by 2030

. For that, conditions have to be gathered, and the decisions that will be taken, especially on additionality, will be crucial to kick-start green H2 production. We also expect strong support from decision makers regarding renewable energy deployment, especially by facilitating and accelerating permits delivery, and strongly promoting Power Purchase Agreement (PPAs), a powerful instrument, in the frame of the RED II revision process; PPAs already represented a total capacity of 11GW in 2020, and all stakeholders agrees to say that’s just the start of a huge growth. We need to encourage them.

5. Combining decarbonization with EU reindustrialization and job creation.

As much as possible, the industrial dimension of the energy transition and the associated value creation should take place in Europe. The EU Green Deal is also a unique opportunity from this point of view. As stressed by the Commission, vulnerabilities of the European energy value chains have to be managed, and value chains creating jobs in Europe must be supported. In this regard, renewable gases (green H2, biomethane) tick all the boxes.

Biomethane for example, respecting high sustainability criteria, can easily achieve 80% greenhouse gas emissions savings compared to fossil fuels, enables circularity, and is a driver for rural development, creating jobs that can hardly be displaced.

Given that potential, biomethane is probably not recognized for its true value, at least for electricity production, in the 55% package.

6. An inclusive transition: leaving no one behind.

The fight against climate change should also embark both the Member States still lagging behind in terms of decarbonization and the most fragile populations. That’s why a sound coherence between the measures contained in the 55% package is highly necessary. Transition will have a cost, regardless of whether this cost is apparent through a price mechanism, such as ETS, or whether it derives from regulatory measures. It needs to be minimized, and care should be taken to the most vulnerable parts of society. As far as possible, the rule of “1 target, 1 instrument” should be applied. This is also one of the conditions for gaining confidence from Member States and populations on new energy solutions, the famous “acceptability”.

7. Never forget security of energy supply.

Although decarbonization must be our absolute compass, security of energy supply should be ensured during and after the transition. This is absolutely essential for all consumers.

Today, firm generating capacities (like coal or nuclear) are being decommissioned – ~70 GW of reliable capacity is expected to disappear in Central-Western Europe and UK between now and 2030 – and intermittent renewable capacities are added into the system.

This creates challenges for the supply-demand equilibrium in real time and for system adequacy across Europe. However, despite the efforts that will be made in terms of energy efficiency, despite the energy imports that will continue, massive capacities will be necessary in the future, even more so if Europe wants to maintain or even develop its industrial potential in the future.

It is the combination of all these factors that will make it possible to achieve the European objective. The EU must be pragmatic ; what matters is reaching the intermediate target of 55% GHG reduction by 2030, in an affordable and resilient way, and getting onto the final trajectory of zero emissions by 2050. ENGIE is committed to contribute to these ambitions.